PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716511

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716511

Reusable Launch Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

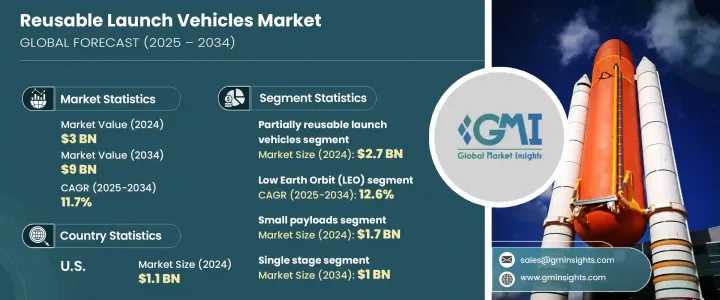

The Global Reusable Launch Vehicles Market generated USD 3 billion in 2024 and is projected to grow at a CAGR of 11.7% between 2025 and 2034. The rising demand for cost-effective and reliable space access is fueling this growth, as reusable launch vehicles (RLVs) offer a more economical alternative to traditional expendable rockets. With the increasing frequency of satellite launches for applications such as communication, Earth observation, navigation, and defense, the need for reusable solutions is becoming more pronounced. These vehicles significantly reduce the cost of space missions by enabling multiple launches with the same hardware, making space exploration and satellite deployment more sustainable and commercially viable.

The growing interest in space tourism and the increasing number of private-sector initiatives in the aerospace industry are also contributing to market growth. Space agencies and private companies alike are investing heavily in developing next-generation RLVs to improve payload capacities, reduce turnaround times, and enhance operational efficiencies. Moreover, advancements in materials, propulsion systems, and AI-driven launch technologies are helping extend the lifespan of reusable components, further driving the adoption of these vehicles. The global market is witnessing increased government and private investments aimed at establishing a robust space infrastructure that supports continuous launches for scientific research, defense, and commercial applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $9 Billion |

| CAGR | 11.7% |

The market for reusable launch vehicles is segmented by vehicle type and orbital range. Vehicle types include partially reusable and fully reusable launch vehicles. Fully reusable launch vehicles are expected to generate USD 1.2 billion by 2034. This segment is still in the early stages of development, with ongoing research and development focused on enhancing turnaround times and minimizing operational costs. As interest in space exploration, satellite mega-constellations, and interplanetary missions grows, fully reusable launch vehicles are poised to offer substantial long-term benefits, including reduced launch costs and faster deployment cycles. Increasing investments in improving thermal shielding, landing systems, and rapid refurbishment processes are accelerating the viability of fully reusable systems for future missions.

The market is also classified by orbit type, including Geostationary Orbit (GEO), Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Beyond Earth Orbit (BEO). The MEO segment held an 8.9% market share in 2024, primarily driven by the increasing demand for secure military communications and the ability of reusable launch vehicles to efficiently deploy large, long-life satellites into these orbits. As military and commercial applications continue to expand, advancements in making MEO more accessible to reusable launch vehicles are expected to stimulate further market growth.

The U.S. reusable launch vehicles market was valued at USD 1.1 billion in 2024, driven by the country's well-established space industry and the presence of leading manufacturers specializing in reusable launch technologies. The growing number of space launch activities in the U.S., coupled with a focus on improving cost-efficiency and reliability, is propelling market growth. With continuous innovation in space exploration and sustained government and private sector investments, the U.S. is expected to remain a global leader in reusable launch vehicle development and adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for satellites orbiting the Earth

- 3.2.1.2 Increasing government and military investments

- 3.2.1.3 Technological advancements in reusability

- 3.2.1.4 Rise of space tourism and suborbital flights

- 3.2.1.5 Increase in space-based manufacturing and research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial development costs

- 3.2.2.2 Limited reusability cycles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Subsystem analysis

- 3.10.1 Guidance, navigation & control systems

- 3.10.2 Propulsion systems

- 3.10.3 Telemetry, tracking & command systems

- 3.10.4 Electrical power systems

- 3.10.5 Others

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Partially reusable launch vehicles

- 5.3 Fully reusable launch vehicles

Chapter 6 Market Estimates and Forecast, By Orbit Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Low Earth Orbit (LEO)

- 6.3 Medium Earth Orbit (MEO)

- 6.4 Geostationary Orbit (GEO)

- 6.5 Beyond Earth Orbit (BEO)

Chapter 7 Market Estimates and Forecast, By Payload Capacity, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Small payloads (up to 2,000 kg)

- 7.3 Medium payloads (2,000 kg to 10,000 kg)

- 7.4 Heavy payloads (above 10,000 kg)

Chapter 8 Market Estimates and Forecast, By Configuration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Single stage

- 8.3 Multi-stage

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Satellite launch

- 9.3 Space exploration

- 9.4 Space tourism

- 9.5 Cargo transport

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Government

- 10.3 Commercial

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Arianespace

- 12.2 Blue Origin

- 12.3 Boeing

- 12.4 China Aerospace Science and Technology Corporation (CASC)

- 12.5 Lockheed Martin

- 12.6 Mitsubishi Heavy Industries

- 12.7 Northrop Grumman

- 12.8 Relativity Space

- 12.9 Rocket Lab

- 12.10 Roscosmos

- 12.11 Sierra Nevada Corporation

- 12.12 SpaceX

- 12.13 Virgin Galactic