PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913396

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913396

High Purity Alumina Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

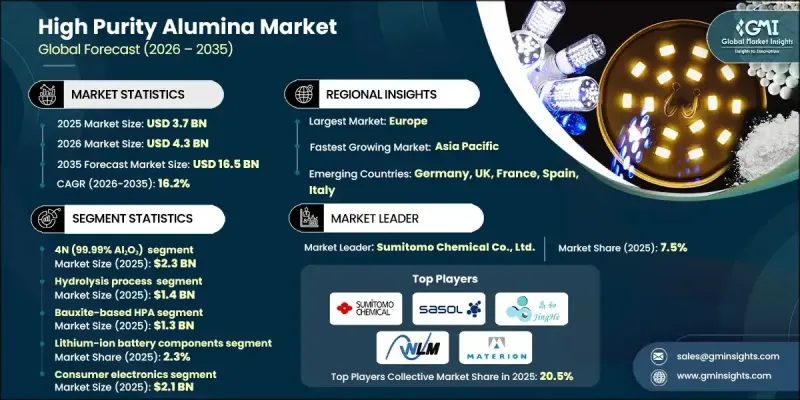

The Global High Purity Alumina Market was valued at USD 3.7 billion in 2025 and is estimated to grow at a CAGR of 16.2% to reach USD 16.5 billion by 2035.

Market growth is driven by rising demand for advanced materials that meet strict quality, reliability, and performance requirements across high-end industrial applications. High purity alumina, derived from aluminum oxide with minimal impurity content, offers excellent thermal stability, strong chemical resistance, and superior electrical insulation properties. These characteristics make it a critical material for applications where precision and durability are essential. Continued reliance on high-performance materials across manufacturing sectors has supported consistent market expansion. Significant improvements in production technologies have also contributed to market momentum, as modernized refining and purification methods now deliver more uniform material quality. Manufacturers are increasingly able to fine-tune material characteristics to meet application-specific requirements while improving energy efficiency and lowering emissions. This evolution reflects the broader industrial shift toward sustainable manufacturing practices and optimized production processes, positioning high purity alumina as a key material in next-generation technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.7 Billion |

| Forecast Value | $16.5 Billion |

| CAGR | 16.2% |

The hydrolysis process segment reached USD 1.4 billion in 2025. Alongside HCl leaching, hydrolysis has gained prominence as a cost-effective and scalable production method capable of delivering consistent purity levels. Its ability to balance large-scale output with strict quality control has made it well-suited to meet growing industrial demand.

The lithium-ion battery components segment held 2.3% share in 2025. Demand for high purity alumina continues to shift toward applications that require exceptional material consistency and reliability. Usage remains strong across sectors that depend on high thermal stability, optical clarity, and minimal contamination, particularly as manufacturing tolerances become increasingly stringent in high-temperature and precision-driven environments.

North America High Purity Alumina Market generated USD 525.3 million in 2025. Growth in this region is supported by strong demand from advanced electronics, aerospace, defense, and energy storage industries. Continued investment in research, innovation, and high manufacturing standards is further accelerating adoption and consumption across the region.

Key companies operating in the Global High Purity Alumina Market include Alcoa Corporation, Baikowski, Norsk Hydro ASA, Materion Corporation, Nippon Light Metal Holdings Co., Ltd., Sumitomo Chemical Co., Ltd., Sasol Limited, Altech Chemicals Limited, Orbite Technologies Inc., PSB Industries SA, Caplinq Corporation, Hebei Pengda Advanced Materials Technology, Xuancheng Jingrui New Materials Co., Ltd., and emerging sustainable HPA producers. Companies in the Global High Purity Alumina Market are strengthening their market position through technology advancement, capacity expansion, and product specialization. Many players are investing in process innovation to achieve higher purity levels while reducing production costs and environmental impact. Strategic focus on application-specific grades allows suppliers to meet evolving customer requirements in electronics, energy storage, and advanced manufacturing. Geographic expansion and localized production are being used to improve supply reliability and reduce logistics risks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Purity Grade

- 2.2.2 Production Technology

- 2.2.3 Raw Material

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for advanced electronics

- 3.2.1.2 Rapid growth in electric vehicle ecosystems

- 3.2.1.3 Expansion of LED and lighting technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and energy requirements

- 3.2.2.2 Competitive pressure from low-cost regional producers

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption in next-generation batteries

- 3.2.3.2 Expansion of 5G and future 6G infrastructure

- 3.2.3.3 Increasing use in aerospace and defence applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By purity grade

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Purity Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 3N (99.9% AL2O3)

- 5.3 4N (99.99% AL2O3)

- 5.4 5N(99.999% AL2O3)

- 5.5 6N (99.9999% AL2O3)

- 5.6 UHPA - ultra high purity alumina (>99.9999%)

Chapter 6 Market Estimates and Forecast, By Production Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Hydrolysis process

- 6.3 HCL (hydrochloric acid) leaching

- 6.4 Alkoxide process

- 6.5 Thermal decomposition

- 6.6 Three-layer electrolytic refining

- 6.7 Fractional crystallization

- 6.8 Vacuum distillation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bauxite-based HPA

- 7.3 Kaolin-based HPA

- 7.4 Aluminum metal-based HPA

- 7.5 High-alumina clay-based HPA

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Led substrates and lighting

- 8.3 Sapphire substrate production

- 8.4 Semiconductor manufacturing

- 8.5 Lithium-ion battery components

- 8.6 5g and telecommunications infrastructure

- 8.7 Medical and biomedical applications

- 8.8 Quantum computing components

- 8.9 Aerospace and defense ceramics

- 8.10 Power electronics and RF devices

- 8.11 Technical ceramics and advanced ceramics

- 8.12 Electronic displays and optoelectronics

- 8.13 Others

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Automotive

- 9.4 Aerospace and defense

- 9.5 Healthcare and medical devices

- 9.6 Telecommunications

- 9.7 Energy and power

- 9.8 Industrial manufacturing

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Alcoa Corporation

- 11.2 Altech Chemicals Limited

- 11.3 Baikowski

- 11.4 Caplinq Corporation

- 11.5 Emerging sustainable HPA producers

- 11.6 Hebei Pengda Advanced Materials Technology

- 11.7 Materion Corporation

- 11.8 Nippon Light Metal Holdings Co., Ltd.

- 11.9 Norsk Hydro ASA

- 11.10 Orbite Technologies Inc.

- 11.11 PSB Industries SA

- 11.12 Sumitomo Chemical Co., Ltd.

- 11.13 Sasol Limited

- 11.14 Xuancheng Jingrui New Materials Co., Ltd.