PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998764

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998764

Osteoporosis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

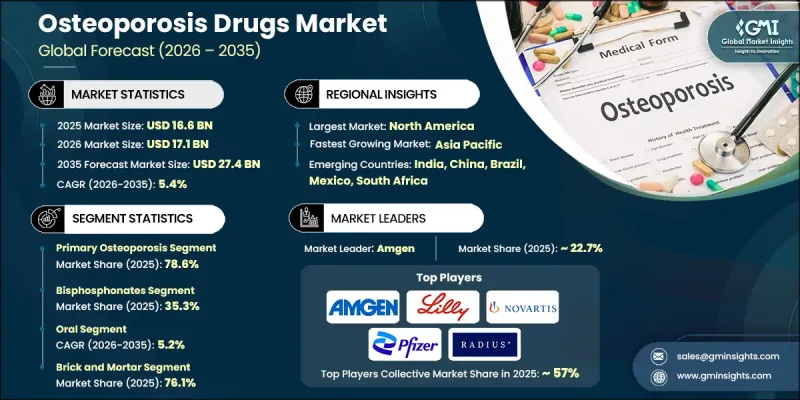

The Global Osteoporosis Drugs Market was valued at USD 16.6 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 27.4 billion by 2035.

The growth of the osteoporosis drugs market is closely associated with demographic changes, particularly the steady expansion of the elderly population worldwide. As individuals age, bone strength gradually declines, which significantly increases the risk of fractures and bone-related complications. Pharmaceutical therapies designed to manage osteoporosis play an essential role in preserving bone density and minimizing fracture risk. These medications function by slowing the process of bone degradation or by stimulating new bone formation, helping patients maintain skeletal strength over time. Increased awareness among patients and healthcare providers has also contributed to improved diagnosis rates, particularly as healthcare systems emphasize early detection of bone loss conditions. The growing use of diagnostic screening technologies is encouraging earlier treatment initiation and expanding the number of patients entering long-term therapy programs. In addition, digital health tools designed to support patient monitoring and treatment adherence are gradually becoming part of routine osteoporosis management. These technologies contribute to better therapeutic outcomes and help healthcare providers track long-term treatment effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.6 Billion |

| Forecast Value | $27.4 Billion |

| CAGR | 5.4% |

The primary osteoporosis segment held 78.6% share in 2025 and is expected to reach USD 22 billion by 2035 while growing at a CAGR of 5.6%. This segment maintains strong demand because bone density loss associated with aging represents the largest source of osteoporosis cases globally. As life expectancy increases across many countries, the number of individuals vulnerable to bone deterioration continues to grow. This demographic trend is generating sustained demand for long-term pharmaceutical interventions designed to preserve bone health. Expanding use of diagnostic screening technologies is also enabling healthcare professionals to detect bone loss at earlier stages, allowing treatment to begin before severe complications occur. Earlier identification of the condition is encouraging more proactive disease management and increasing the overall patient population receiving osteoporosis therapies.

The oral segment generated USD 9.1 billion in 2025 and is projected to grow at a CAGR of 5.2% throughout 2026-2035. Oral drug formulations remain widely used because they are convenient for patients and easily distributed through multiple healthcare channels. Their accessibility across both developed and developing healthcare systems ensures stable and consistent market demand. Healthcare professionals continue to prescribe oral osteoporosis medications due to their well-established therapeutic effectiveness in supporting bone health and lowering the likelihood of fracture-related complications. The extensive clinical history associated with oral treatments has strengthened physician confidence in these therapies and contributed to their continued adoption worldwide.

U.S. Osteoporosis Drugs Market reached USD 5.7 billion in 2025. Osteoporosis-related conditions remain common among the aging population in North America, contributing to the growing need for long-term pharmaceutical treatment. Rising life expectancy is expanding the number of patients who require continued management of bone health conditions. Increased awareness initiatives and physician-led screening programs have also improved early detection and encouraged the use of preventive treatment options. In addition, advanced healthcare infrastructure and strong availability of diagnostic technologies continue to support effective disease management across the region.

Prominent companies operating in the Global Osteoporosis Drugs Market include Amgen, Apotex, DAIICHI SANKYO COMPANY, Dr. Reddy's Laboratories, Eisai, Eli Lilly and Company, Merck & Co., Mylan, Novartis, Pfizer, Radius Health, Roche, Sanofi, Sun Pharmaceutical Industries, and Teva Pharmaceutical Industries. Companies competing in the Global Osteoporosis Drugs Market are strengthening their competitive position through a combination of product innovation, research investments, and strategic collaborations. Many pharmaceutical manufacturers are increasing funding for clinical research to develop next-generation therapies that improve treatment outcomes and support long-term bone health management. Organizations are also expanding their global distribution networks to increase product availability across emerging healthcare markets. Partnerships with healthcare providers and research institutions are helping companies accelerate drug development and improve patient access to therapies. Additionally, firms are focusing on digital health integration to support medication adherence and patient monitoring.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of osteoporosis

- 3.2.1.2 Technological advancements in drug development

- 3.2.1.3 Rising incidence of fractures

- 3.2.1.4 Growth in biologic and novel therapeutic adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects and safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation anabolic agents

- 3.2.3.2 Biosimilar and biobetter entry

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Value chain analysis

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Start-up scenarios

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Primary osteoporosis

- 5.2.1 Postmenopausal osteoporosis

- 5.2.2 Senile osteoporosis

- 5.2.3 Idiopathic osteoporosis

- 5.3 Secondary osteoporosis

Chapter 6 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Bisphosphonates

- 6.3 RANK ligand inhibitors

- 6.4 Parathyroid hormone analogs

- 6.5 Hormone replacement therapy (HRT)

- 6.6 Selective estrogen receptor modulators (SERMs)

- 6.7 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Other route of administrations

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Brick and mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amgen

- 10.2 Apotex

- 10.3 DAIICHI SANKYO COMPANY

- 10.4 Dr. Reddy’s Laboratories

- 10.5 Eisai

- 10.6 Eli Lilly and Company

- 10.7 Merck & Co.

- 10.8 Mylan

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Radius Health

- 10.12 Roche

- 10.13 Sanofi

- 10.14 Sun Pharmaceutical Industries

- 10.15 Teva Pharmaceutical Industries