PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716604

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1716604

Auto Dealership Accounting Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

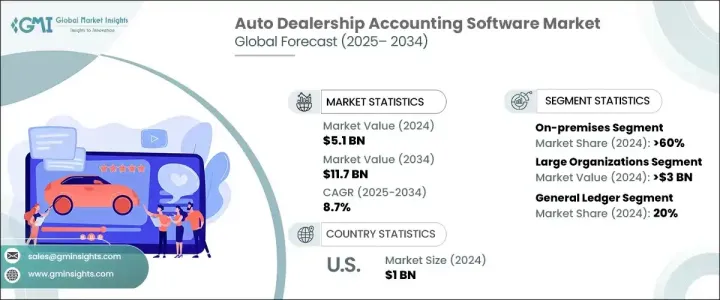

The Global Auto Dealership Accounting Software Market reached USD 5.1 billion in 2024 and is projected to grow at a CAGR of 8.7% from 2025 to 2034. A primary driver fueling this growth is the widespread adoption of cloud-based accounting solutions. Dealerships are rapidly transitioning to cloud platforms to enhance operational efficiency, streamline financial processes, and gain real-time access to crucial business data. With the increasing complexity of financial management in the auto industry, businesses are prioritizing accounting software that integrates seamlessly with dealer management systems (DMS). This shift allows dealerships to automate tax calculations, payroll processing, expense tracking, and compliance management while reducing manual errors and operational costs. Additionally, cloud-based solutions are highly scalable, enabling dealerships to expand their operations without significant infrastructure investments.

The rising preference for data-driven decision-making is another factor propelling market expansion. Auto dealerships are leveraging advanced analytics and artificial intelligence (AI) features embedded within modern accounting software to gain insights into sales trends, customer purchasing behavior, and inventory turnover. The growing demand for AI-powered automation tools is accelerating software adoption, helping businesses optimize their financial workflows. As digital transformation takes center stage, software providers are integrating machine learning algorithms and predictive analytics to offer enhanced financial forecasting and risk assessment capabilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $11.7 Billion |

| CAGR | 8.7% |

The market is segmented by deployment mode into cloud-based and on-premises solutions. While cloud-based systems are gaining traction, on-premises solutions held a dominant 60% market share in 2024. Many dealerships prefer on-premises accounting software due to heightened security concerns and the ability to maintain full control over sensitive financial data. Industries such as automotive sales, healthcare, and financial services prioritize stringent data protection measures, making on-premises solutions a preferred choice despite the increasing shift toward cloud technology.

Based on organization size, the market is categorized into large enterprises and small to medium enterprises (SME ). Large dealerships accounted for USD 3 billion in revenue in 2024, largely due to their financial capability to invest in advanced accounting and dealer management software. These enterprises operate extensive dealership networks that require integrated solutions for managing inventory, sales, customer relationships, and compliance. By leveraging comprehensive accounting systems, large organizations can enhance transparency, improve cash flow management, and optimize business performance.

North America dominated the auto dealership accounting software market with a 34% share in 2024, led by the United States. The country's advanced infrastructure, strong economy, and the presence of leading software firms contribute to the growing demand for sophisticated accounting solutions. Regulatory frameworks in the U.S. push businesses toward adopting compliant financial management systems, further driving market growth. With the increasing adoption of cloud-based and AI-driven accounting solutions, North American dealerships are at the forefront of digital financial transformation, ensuring operational efficiency and long-term business sustainability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Software providers

- 3.1.1.2 Service providers

- 3.1.1.3 Technology providers

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Use cases

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing adoption of cloud-based accounting solutions

- 3.6.1.2 Growing demand for automation in financial management

- 3.6.1.3 Stringent regulatory compliance and tax reporting requirements

- 3.6.1.4 Integration with Customer Relationship Management (CRM) and Enterprise Resource Planning (ERP) systems

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High implementation and maintenance costs

- 3.6.2.2 Data security and cybersecurity concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Software, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 General ledger

- 5.3 Inventory management

- 5.4 Accounts payable and receivable

- 5.5 Payroll management

- 5.6 Financial reporting and analysis

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Organization size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large organization

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Autosoft

- 9.2 Autpraptor

- 9.3 CAMS

- 9.4 CDK Global

- 9.5 DealerBuilt

- 9.6 DealerSocket

- 9.7 Fishbowl

- 9.8 Frazer

- 9.9 FreshBooks

- 9.10 Intuit

- 9.11 LBMC

- 9.12 MYOB

- 9.13 NetSuite

- 9.14 PBS Systems

- 9.15 Procede Software

- 9.16 Reynolds and Reynolds

- 9.17 RouteOne LLC

- 9.18 Sage Group

- 9.19 SAP SE

- 9.20 Xero