PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936644

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936644

Joint Pain Injections Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

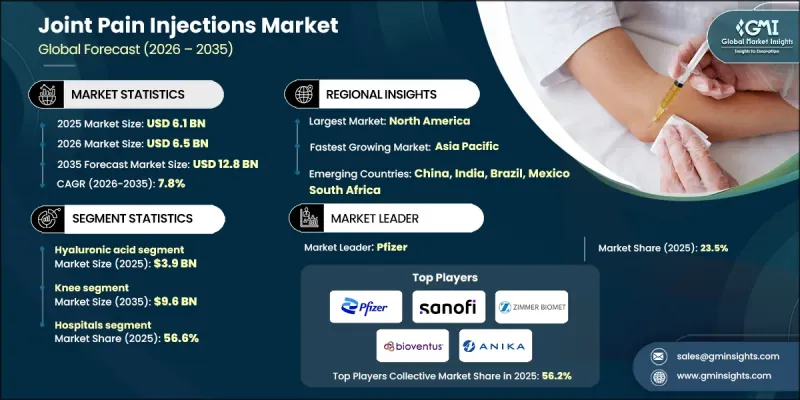

The Global Joint Pain Injections Market was valued at USD 6.1 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 12.8 billion by 2035.

Market growth is supported by the increasing global burden of musculoskeletal disorders, which remain a major cause of long-term disability and reduced quality of life. As joint-related conditions increasingly limit mobility and daily function, demand continues to rise for treatment options that offer pain relief without surgical intervention. Joint pain injections represent minimally invasive therapies designed to reduce inflammation, relieve discomfort, and restore joint movement in patients affected by degenerative and injury-related conditions. The market is steadily shifting toward advanced regenerative and biologic injection solutions that focus on tissue repair and functional recovery rather than short-term symptom control. Positive clinical outcomes and improved patient mobility have strengthened confidence in these therapies. Growth is further supported by rising arthritis prevalence among aging populations and increasing joint injuries among physically active individuals. Younger patients are also adopting injectable treatments to maintain activity levels and postpone surgical procedures, broadening the market beyond traditional age-related use.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.1 Billion |

| Forecast Value | $12.8 Billion |

| CAGR | 7.8% |

The hyaluronic acid segment reached USD 3.9 billion in 2025. This segment maintains a strong position due to its established role in improving joint lubrication, minimizing friction, and enhancing movement in degenerative joint conditions. Its favorable safety profile, strong clinical acceptance, and broad availability across healthcare settings continue to support widespread adoption. Increasing diagnosis rates of joint degeneration further reinforce the sustained demand for hyaluronic acid-based injection therapies.

The knee segment is projected to reach USD 9.6 billion by 2035. This growth is driven by the rising occurrence of knee joint degeneration associated with aging populations, lifestyle-related factors, and metabolic health conditions. High treatment volumes and the availability of multiple injectable therapy options have positioned the knee as the most frequently treated joint, strengthening its dominance across clinical practices and outpatient care facilities.

North America Joint Pain Injections Market accounted for 47.1% share in 2025, maintaining its position as the leading regional market. This dominance is supported by a large patient base affected by joint disorders, advanced healthcare infrastructure, and widespread use of innovative injection therapies. Favorable reimbursement frameworks, high healthcare spending, strong patient awareness, and early adoption of non-surgical treatment approaches continue to drive market growth across the region. The presence of major industry participants further enhances regional leadership.

Key companies operating in the Joint Pain Injections Market include Zimmer Biomet Holdings, Sanofi, Pfizer, Stryker Corporation, Anika Therapeutics, SEIKAGAKU CORPORATION, Bioventus, Arthrex, OrthogenRx, Lifecore Biomedical, Pacira BioSciences (Flexion), Emcyte Corporation, Cipla, and Ferring. Companies in the joint pain injections market are implementing targeted strategies to strengthen market positioning and sustain growth. Significant investments are being made in research and development to advance biologic and regenerative injection technologies with improved clinical outcomes. Strategic collaborations with healthcare providers and orthopedic specialists are expanding treatment accessibility and clinical adoption. Firms are also focusing on portfolio diversification to address multiple joint types and disease stages. Geographic expansion into emerging markets and strengthening distribution networks remain key priorities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Injection type trends

- 2.2.3 Joint type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of osteoarthritis and musculoskeletal disorders

- 3.2.1.2 Growing adoption of minimally invasive and non-surgical therapies

- 3.2.1.3 Advancements in biologic and regenerative therapies

- 3.2.1.4 Rising awareness and healthcare access

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of adverse reactions and variable efficacy

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of orthobiologic therapies

- 3.2.3.2 Growing demand for personalized and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Joint pain epidemiology scenario

- 3.8 Pipeline analysis

- 3.9 Pricing analysis

- 3.10 Future market trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Injection Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hyaluronic acid injections

- 5.3 Corticosteroid injections

- 5.4 Platelet rich plasma injections

- 5.5 Other injection types

Chapter 6 Market Estimates and Forecast, By Joint Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Knee

- 6.3 Shoulder and elbow

- 6.4 Ankle and hip

- 6.5 Other joint types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic/pain clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anika Therapeutics

- 9.2 Arthrex

- 9.3 Bioventus

- 9.4 Cipla

- 9.5 Emcyte Corporation

- 9.6 Ferring

- 9.7 Lifecore Biomedical

- 9.8 OrthogenRx

- 9.9 Pacira BioSciences (Flexion)

- 9.10 Pfizer

- 9.11 Sanofi

- 9.12 SEIKAGAKU CORPORATION

- 9.13 Stryker Corporation

- 9.14 Zimmer Biomet Holdings