PUBLISHER: China Research and Intelligence | PRODUCT CODE: 1578768

PUBLISHER: China Research and Intelligence | PRODUCT CODE: 1578768

Thailand Steel Industry Research Report 2024-2033

Thailand is the second largest economy in ASEAN after Indonesia, with a total land area of 513,120 square kilometers. As of the end of 2023, Thailand has a population of approximately 70 million.

INFOGRAPHICS

Thailand has an annual steel production capacity of about 10 million tons, mainly using the electric arc furnace (EAF) production process. The major steel companies in Thailand are GSteel Steel, GJSteel Steel, and Tata Steel Thailand. In December 2021, Nippon Steel announced that it had paid US$419 million to acquire a 49.99% stake in GSteel Steel and a 40.45% stake in GJSteel Steel. As of now, no new capacity expansion projects have been announced by Thai officials.

Considering efficiency and cost issues, the equipment utilization rate of Thai steel companies is not very high. Thailand's domestic demand for flat steel is mainly met through imports (70%-75% of total imports). Japan, China and South Korea are Thailand's top three sources of imports, while the US, Indonesia and Vietnam are its top three export destinations.

Thailand is not very rich in raw material resources; its iron ore production is very small and it relies mainly on imports. Phu Ang Iron Ore Mine located in Lai Phu, Thailand is the largest iron ore mine in Thailand, with total reserves estimated at 10.9 million tons and an iron content of 65% to 67%. Another mine in Thailand is the Phu Hia iron ore mine. Both of these iron ore mines are located in northeastern Thailand.

Thai steelmakers are worried about the influx of cheap steel products from Russia into the Thai and ASEAN markets after Russia was sanctioned over the Russia-Ukraine war. Russia is looking for new buyers as its steel exports are banned from the European market. Meanwhile, Chinese steelmakers are also seeking to expand exports as steel consumption in China has fallen. If cheap imported steel products are dumped into the Thai market, it is expected to deal a devastating blow to Thailand's domestic steel manufacturing industry.

In recent years, Thailand's steel consumption has been more than 60% dependent on imported steel. In 2018, this figure was 62.3%, rising to nearly 69% by 2023.

For example, in 2023, Thailand's apparent consumption of finished steel was about 16.33 million tons, and in that year, Thailand's production volume of finished steel was only 6.6 million tons, and import volume of finished steel was as high as 11.21 million tons.

As a result, some local Thai steel manufacturers have asked the Thai government to restrict steel imports. For more than a decade, the Thai government has issued a series of anti-dumping measures against imported steel products, but they have been largely ineffective. The main reason for Thailand's rising steel imports is the high cost of Thai-produced steel, as well as an inadequate product range. For downstream companies, it is more cost-effective to purchase imported products. Thai steel imports will continue to rise in the future if Thai steel companies do not seek to reduce production costs and develop mid-range and high-end products.

In 2023, Thailand's consumption of finishes steel declined 0.4% year-on-year to 16.33 million tons from 16.39 million tons in 2022. The CAGR of consumption of finished steel in Thailand is -3.3% over the period 2018-2023.

As the cost of crude steel and steel production in Thailand is higher than in some countries in Southeast Asia, such as Vietnam and Indonesia, and also higher than in China, India and Japan in Asia, the growth of Thailand's domestic steel output volume is expected to be limited in the next few years. In case of low steel prices in the international market, there is a possibility of a decline in Thailand's domestic steel production.

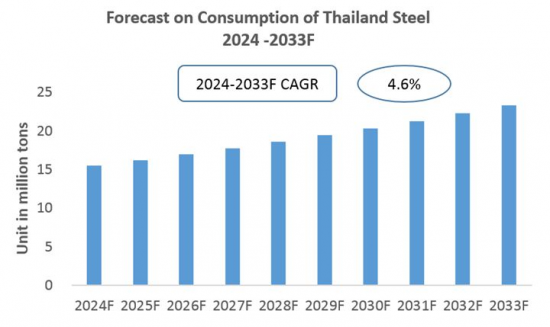

CRI predicts that Thailand's steel production and consumption will both increase in 2024-2033. The main reason is that Thailand is the country with the strongest comprehensive manufacturing strength in Southeast Asia. On the one hand, the continued growth of Thailand's economy will promote the increase in Thailand's domestic steel consumption. At the same time, with the economic growth of other Southeast Asian countries such as Vietnam, Thailand's steel exports to these countries are expected to increase.

Factors such as the Sino-US trade war will reduce China's steel exports, which will be beneficial to the development of Thailand's local steel industry to a certain extent.

Topics covered:

Thailand Steel Industry Overview

The economic and policy environment of Thailand's steel industry

Thailand Steel Industry Market Size, 2024-2033

Analysis of the main Thailand's steel production enterprises

Key drivers and market opportunities for Thailand's steel industry

What are the key drivers, challenges and opportunities for Thailand's steel industry during the forecast period 2024-2033?

Which companies are the key players in the Thailand steel industry market and what are their competitive advantages?

What is the expected revenue of Thailand steel industry market during the forecast period 2024-2033?

What are the strategies adopted by the key players in the market to increase their market share in the industry?

Which segment of the Thailand steel industry market is expected to dominate the market by 2032?

What are the main negative factors facing the steel industry in Thailand?

Table of Contents

1 Development Environment of Thailand Steel Industry

- 1.1 Economic Environment

- 1.1.1 Thailand's Economy

- 1.1.2 Foreign Investment in Thailand Steel Industry

- 1.1.3 Minimum Wage Standard in Thailand

- 1.1.4 The impact of COVID-19 on Thailand's Steel Industry

- 1.2 Policy Environment

- 1.2.1 Policies Related to Steel Industry

- 1.2.2 Preferential Policies on Foreign Investment

- 1.2.3 Anti-dumping measures

- 1.3 Research Methods of the Report

- 1.3.1 Parameters and Assumptions

- 1.3.2 Data Sources

- 1.3.3 About CRI

2 Market Status of Thailand Steel Industry, 2018-2023

- 2.1 Supply

- 2.1.1 Production Capacity

- 2.1.2 Production Volume

- 2.1.2 Production Volume

- 2.2 Demand on Thailand Steel Market

- 2.2.1 Total Demand

- 2.2.2 Demand Structure

- 2.2.3 Steel Price

- 2.3 Competition Structure of Thailand Steel Market

- 2.3.1 Upstream Suppliers

- 2.3.2 Downstream Customers

- 2.3.3 Competition in Steel Industry

- 2.3.4 Potential Entrants

- 2.3.5 Substitutes

3 Major steel products in Thailand

- 3.1 Flat steel products industry

- 3.1.1 Supply and Production Volume

- 3.1.2 Demand

- 3.1.3 Imports and Exports

- 3.2 Long steel products

- 3.2.1 Supply and Production Volume

- 3.2.2 Demand

- 3.2.3 Imports and Exports

- 3.3 Steel pipes

4 Analysis on Import and Export of Steel in Thailand, 2018-2023

- 4.1 Import

- 4.1.1 Import Overview

- 4.1.2 Major Import Sources

- 4.2 Export

- 4.2.1 Export Overview

- 4.2.2 Export Destinations

5 Major Steel Manufacturers in Thailand, 2018-2023

- 5.1 Sahaviriya Steel Industries PCL

- 5.2 G Steel Public Company Limited

- 5.3 G J Steel PCL

- 5.4 Tata Steel (Thailand) Public Company Limited Group

- 5.5 Bangkok Steel Industry Public Co., Ltd.

- 5.6 Prime Steel Mill Co., Ltd.

- 5.7 LPN Plate Mill Ltd.

- 5.8 Asia Metal Plc.

- 5.9 2S Metal Plc.

- 5.10 Thai Cold Rolled Steel Sheet Plc.

- 5.11 The Steel Plc.

- 5.12 TMT Steel Plc.

6 Prospect of Thailand Steel Market, 2024-2033

- 6.1 Factors Influencing Development

- 6.1.1 Market Opportunities and Driving Forces

- 6.1.2 Threats and Challenges

- 6.2 Forecast on Supply and Demand

- 6.2.1 Forecast on Production Volume

- 6.2.2 Forecast on Demand

- 6.2.3 Forecast on Import and Export

- 6.3 Analysis on Investment Opportunities in Thailand Steel Industry

Disclaimer

Service Guarantees

LIST OF CHARTS

- Chart Location of Thailand in Southeast Asia

- Chart Thailand GDP per capita 2013-2023

- Chart Minimum Daily Wage in Thailand 2013-2024

- Chart Thailand's steel import volume as a percentage of steel consumption

- Chart Output Volume of Crude Steel in Thailand, 2018-2023

- Chart Output Volume of Finished Steel in Thailand, 2018-2023

- Chart Demand Volume of Finished Steel in Thailand, 2018-2023

- Chart Demand Structure of Steel in Thailand in 2023

- Chart Price Index of Thailand Import Steel

- Chart Output Volume of Flat Steel in Thailand, 2018-2023

- Chart Demand Volume of Flat Steel in Thailand, 2018-2023

- Chart Import Volume of Flat Steel in Thailand, 2018-2023

- Chart Export Volume of Flat Steel in Thailand, 2018-2023

- Chart Output Volume of Long Steel in Thailand, 2018-2023

- Chart Demand Volume of Long Steel in Thailand, 2018-2023

- Chart Import Volume of Long Steel in Thailand, 2018-2023

- Chart Export Volume of Long Steel in Thailand, 2018-2023

- Chart Import Volume of Finished Steel in Thailand, 2018-2023

- Chart Export Volume of Finished Steel in Thailand, 2018-2023

- Chart Profile of Sahaviriya Steel Industries PCL

- Chart Profile of G Steel Public Company Limited

- Chart Profile of G J Steel PCL

- Chart Profile of Tata Steel (Thailand) Public Company Limited Group

- Chart Profile of Bangkok Steel Industry Public Co., Ltd.

- Chart Profile of Prime Steel Mill Co., Ltd.

- Chart Profile of LPN Plate Mill Plc.

- Chart Forecast on Output Volume of Thailand Steel 2024-2033

- Chart Forecast on Consumption of Thailand Steel 2024-2033

- Chart Forecast on Import Volume of Thailand Steel 2024-2033

- Chart Forecast on Export Volume of Thailand Steel 2024-2033