PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1706588

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1706588

Global Military Communication Market 2025-2035

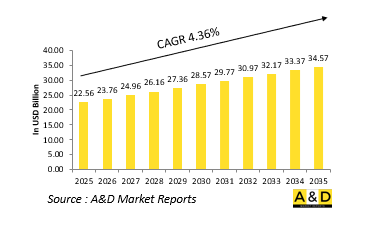

The Global Military Communication market is estimated at USD 22.56 billion in 2025, projected to grow to USD 34.57 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 4.36% over the forecast period 2025-2035.

Introduction to Military Communication Market:

Military communication systems are the lifelines of command and control (C2) on the modern battlefield. These systems enable the secure, rapid, and reliable exchange of data, voice, video, and imagery between forces across different domains-land, sea, air, space, and cyberspace. From satellite uplinks and tactical radios to secure internet protocols and battlefield messaging platforms, military communication is the connective tissue that links decision-makers, combat units, and support elements into a cohesive fighting force. Historically, military communication evolved from flag signals and wire-based telegraphy to sophisticated encrypted networks and digital transmission systems. In the current strategic environment, the emphasis is on interoperability, resilience, and real-time connectivity across multiple platforms and coalition partners. Whether coordinating airstrikes, navigating unmanned systems, or monitoring cyber defense, communication capabilities now determine operational effectiveness as much as weapon systems themselves. As threats become more dispersed and multidimensional-from near-peer adversaries to asymmetric actors-military forces are under increasing pressure to maintain robust, adaptive communication networks that function across contested electromagnetic spectrums and cyber-compromised zones. The growing adoption of network-centric warfare, joint-force doctrines, and multi-domain operations has elevated military communication from a tactical support function to a core pillar of defense strategy.

Technology Impact in Military Communication Market:

Recent technological advancements have transformed military communication into a highly agile, intelligent, and data-centric domain. One of the most disruptive changes is the shift toward Software-Defined Radios (SDRs). These radios replace hardware-dependent communication systems with flexible software that can dynamically switch frequencies, modulation types, and encryption protocols. SDRs allow units to interconnect even when using different systems or operating under spectrum constraints, boosting mission adaptability.

5G and edge computing are emerging as significant enablers of low-latency, high-bandwidth data exchange. These technologies allow for real-time data fusion and transmission in dense environments, enabling everything from live drone feeds to augmented reality (AR) combat overlays and IoT-enabled logistics tracking. The combination of 5G and edge processing reduces reliance on centralized command centers and allows frontline units to process and act on data independently. Another game-changing development is the integration of Low Earth Orbit (LEO) satellite constellations, which are redefining secure global coverage and redundancy. Unlike traditional geostationary satellites, LEO networks-such as those deployed by Starlink and OneWeb-offer lower latency, faster data throughput, and improved coverage in polar and remote regions. Militaries are rapidly exploring LEO integration for uninterrupted C2 during peer conflict scenarios.

The impact of Artificial Intelligence (AI) in military communication cannot be overstated. AI-powered systems are now used to optimize bandwidth usage, detect anomalies in communication patterns, and even automate message translation across languages and encryption schemes. Intelligent communication routing ensures that data takes the fastest, most secure path, minimizing vulnerabilities. Additionally, Quantum communication and post-quantum encryption are being explored for ultra-secure channels immune to conventional cyber interception. These cutting-edge technologies are still in their nascent stages but are attracting significant investment as defense establishments prepare for the advent of quantum computing threats. Meanwhile, cybersecurity technologies are being built directly into communication architectures. End-to-end encryption, zero-trust frameworks, and dynamic access controls are vital for maintaining operational security. As military networks face increasing cyber threats from state and non-state actors, secure communication channels have become a critical area of technological focus.

Key Drivers in Military Communication Market:

Several strategic and operational factors are propelling the evolution and expansion of global military communication systems. Chief among them is the need for seamless multi-domain operations. Modern warfare demands coordination between land, sea, air, space, and cyber forces-often in real time. Communication networks must support synchronized efforts across these domains to ensure mission success. The rise of joint and coalition operations is another major driver. Most modern military engagements involve multi-national forces, requiring interoperability across disparate systems and doctrines. This has led to the development of standardized protocols like NATO's Federated Mission Networking (FMN), which supports data sharing and secure communications among allied forces.

Another important factor is the increasing complexity of battlefield assets. With unmanned systems, sensors, and weapon platforms generating vast amounts of data, there is a growing demand for high-speed, secure data pipelines that can move, process, and interpret information at the tactical edge. This has also driven interest in mesh networking and intelligent bandwidth management. Situational awareness and rapid decision-making are further amplifying demand. Commanders now require live feeds from multiple sensors, troop trackers, and ISR platforms to make informed decisions. This pushes communication systems to prioritize data fusion, real-time analytics, and resilience under pressure.

Moreover, the growing threat from electronic warfare (EW) and cyber-attacks is influencing communication strategies. Adversaries now target military networks with jamming, spoofing, and hacking techniques to disrupt or degrade communications. This has led to increased investment in anti-jamming technologies, frequency agility, and cyber-hardened transmission protocols. Budgetary considerations also play a role. Many nations are balancing the need for cutting-edge communication systems with pressure to reduce lifecycle costs and minimize dependence on proprietary platforms. This drives the adoption of open standards, modular upgrades, and commercial off-the-shelf (COTS) components that can be ruggedized for military use.

Regional Trends in Military Communication Market:

The global military communication landscape is shaped by regional defense priorities, threat perceptions, and technological capabilities.

In North America, particularly the United States, the focus is on achieving full-spectrum dominance through resilient and unified communication architectures. Programs like the Joint All-Domain Command and Control (JADC2) aim to integrate forces across domains via AI-powered data sharing and secure communications. The U.S. military is heavily investing in LEO satellite networks, spectrum management, and AI-driven cybersecurity to ensure strategic edge over peer rivals. Canada is similarly upgrading its communication infrastructure for interoperability with U.S. and NATO forces, especially in Arctic and maritime domains. Europe is concentrating on enhancing interoperability among NATO members and modernizing legacy systems. Initiatives like the European Secure Software Defined Radio (ESSOR) project and the development of pan-European military satcom capabilities reflect this trend. France, Germany, and the UK are leading the charge with investments in tactical communications, battlefield networking, and sovereign satellite capabilities. The war in Ukraine has also prompted many countries to accelerate secure communication deployments to guard against electronic warfare. In Asia-Pacific, regional tensions and military modernization programs are fueling rapid advances in communication technologies. China is pursuing indigenous, cyber-resilient communication systems with integrated satellite, terrestrial, and HF (high frequency) channels to ensure operational continuity. India is investing in network-centric warfare and satellite-based C2 systems as part of its modernization initiatives, including the Defense Space Agency's efforts. Japan and South Korea are enhancing their battlefield communication infrastructure to deter regional threats and support U.S.-led joint operations.

Key Military Communication Program:

On February 20, 2025, the Ministry of Defence signed a contract with Bharat Electronics Limited (BEL), Bengaluru, for the procurement of 149 Software Defined Radios (SDRs) for the Indian Coast Guard. Valued at ₹1,220.12 crore, the acquisition falls under the Buy (Indian-IDDM) category. These advanced SDRs are designed to provide secure, high-speed data and voice communication, enhancing information sharing, operational coordination, and situational awareness. Their integration will significantly boost the Indian Coast Guard's capabilities in key mission areas such as maritime law enforcement, search and rescue, fisheries protection, and marine environmental safeguarding. The radios will also improve interoperability with the Indian Navy during joint operations. This initiative represents a strategic move to enhance the Coast Guard's operational readiness while supporting the Government of India's Blue Economy goals by strengthening maritime security. In line with the Atmanirbhar Bharat vision, the project will also contribute to the development of indigenous capabilities in military-grade communication technologies, promote local manufacturing, create employment opportunities, and foster skill development in the defense sector.

Gilat Satellite Networks Ltd, a global leader in satellite networking technologies and services, has announced that its Defense Division has secured a $6 million order to supply its SkyEdge II-c platform to a military organization in the Asia-Pacific region. The advanced satellite communications solution will support both stationary and mobile operations, delivering secure and reliable connectivity for critical defense missions, with enhanced cyber protection at the air interface level.

Table of Contents

Military Communication Market Report Definition

Military Communication Market Segmentation

By Region

By Component

By End-User

Military Communication Market Analysis for next 10 Years

The 10-year Military Communication Market analysis would give a detailed overview of Military Communication Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Military Communication Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Military Communication Market Forecast

The 10-year Military Communication Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Military Communication Market Trends & Forecast

The regional Military Communication Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Military Communication Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Military Communication Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Military Communication Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By End User, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

List of Figures

- Figure 1: Global Military Communication Market Forecast, 2025-2035

- Figure 2: Global Military Communication Market Forecast, By Region, 2025-2035

- Figure 3: Global Military Communication Market Forecast, By End User, 2025-2035

- Figure 4: Global Military Communication Market Forecast, By Type, 2025-2035

- Figure 5: North America, Military Communication Market, Market Forecast, 2025-2035

- Figure 6: Europe, Military Communication Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Military Communication Market, Market Forecast, 2025-2035

- Figure 8: APAC, Military Communication Market, Market Forecast, 2025-2035

- Figure 9: South America, Military Communication Market, Market Forecast, 2025-2035

- Figure 10: United States, Military Communication Market, Technology Maturation, 2025-2035

- Figure 11: United States, Military Communication Market, Market Forecast, 2025-2035

- Figure 12: Canada, Military Communication Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Military Communication Market, Market Forecast, 2025-2035

- Figure 14: Italy, Military Communication Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Military Communication Market, Market Forecast, 2025-2035

- Figure 16: France, Military Communication Market, Technology Maturation, 2025-2035

- Figure 17: France, Military Communication Market, Market Forecast, 2025-2035

- Figure 18: Germany, Military Communication Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Military Communication Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Military Communication Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Military Communication Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Military Communication Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Military Communication Market, Market Forecast, 2025-2035

- Figure 24: Spain, Military Communication Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Military Communication Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Military Communication Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Military Communication Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Military Communication Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Military Communication Market, Market Forecast, 2025-2035

- Figure 30: Australia, Military Communication Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Military Communication Market, Market Forecast, 2025-2035

- Figure 32: India, Military Communication Market, Technology Maturation, 2025-2035

- Figure 33: India, Military Communication Market, Market Forecast, 2025-2035

- Figure 34: China, Military Communication Market, Technology Maturation, 2025-2035

- Figure 35: China, Military Communication Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Military Communication Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Military Communication Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Military Communication Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Military Communication Market, Market Forecast, 2025-2035

- Figure 40: Japan, Military Communication Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Military Communication Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Military Communication Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Military Communication Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Military Communication Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Military Communication Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Military Communication Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Military Communication Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Military Communication Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Military Communication Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Military Communication Market, By End User (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Military Communication Market, By End User (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Military Communication Market, By Type (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Military Communication Market, By Type (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Military Communication Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Military Communication Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Military Communication Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Military Communication Market, By Region, 2025-2035

- Figure 58: Scenario 1, Military Communication Market, By End User, 2025-2035

- Figure 59: Scenario 1, Military Communication Market, By Type, 2025-2035

- Figure 60: Scenario 2, Military Communication Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Military Communication Market, By Region, 2025-2035

- Figure 62: Scenario 2, Military Communication Market, By End User, 2025-2035

- Figure 63: Scenario 2, Military Communication Market, By Type, 2025-2035

- Figure 64: Company Benchmark, Military Communication Market, 2025-2035